Credit and your mortgage

As we move forward with clarity and hope, I encourage you to look at the reality of your finances. The team at Mortgage Allies understand that getting a mortgage can feel overwhelming and confusing, and that’s why we want to empower you with information that matters. When it comes to your credit, it’s important to be clear about where you’re at. Last month we covered a webinar titled ‘Credit & Your Mortgage’. Jump right in to watch the recording and check out the summary!

The way that lenders measure credit for mortgage eligibility has evolved substantially over the years. From a scoreless system of your mortgage broker “selling” your credit worthiness to a mortgage lender, to today where your credit worthiness is captured on a report readily accessible to any lender willing to purchase your data with your consent.

Your credit report provides mortgage lenders with a Fair Isaac Corporation (FICO) Score (“Credit Score”), a list of your liabilities, payment history (including delinquencies), your home address history, employment history, lending risk scores, etc.

Credit reports have made it much easier for lenders to assess mortgage applicants, but the credit report with its all-important FICO score has also largely removed the borrower’s ability to explain any circumstances that may have led to poor credit. Despite its importance and the consequences associated with incorrect or damaged credit, it is hard to believe that financial institutions are not mandated to teach and inform borrowers about credit their credit.

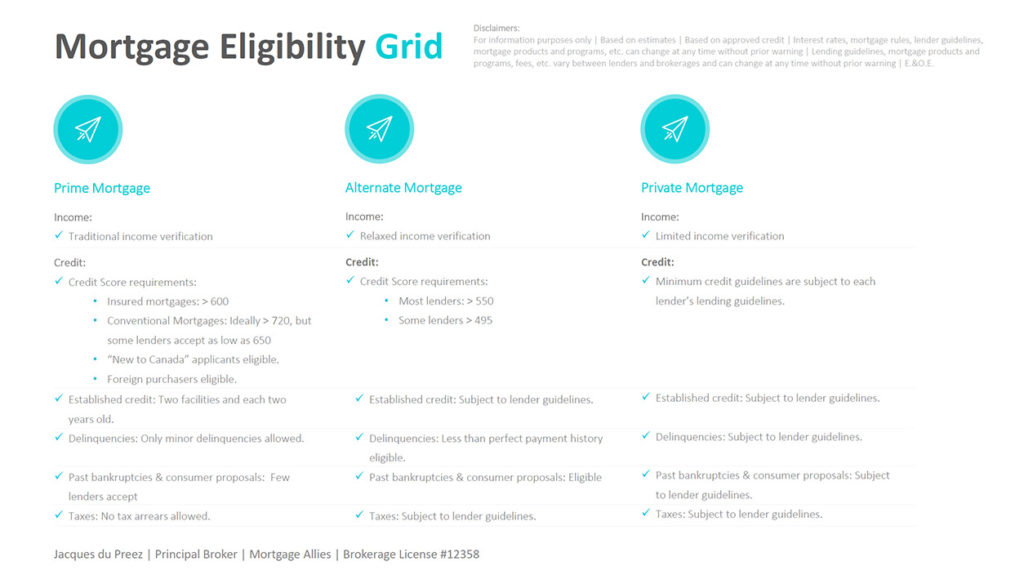

Even though credit is one of the top 5 mortgage eligibility criteria, and the consequences of damaged credit can be very costly, no one is responsible to teach you about credit. It is important that you understand what drives your credit, and how to manage it. This will ensure that you have the best likelihood of getting an excellent prime mortgage.

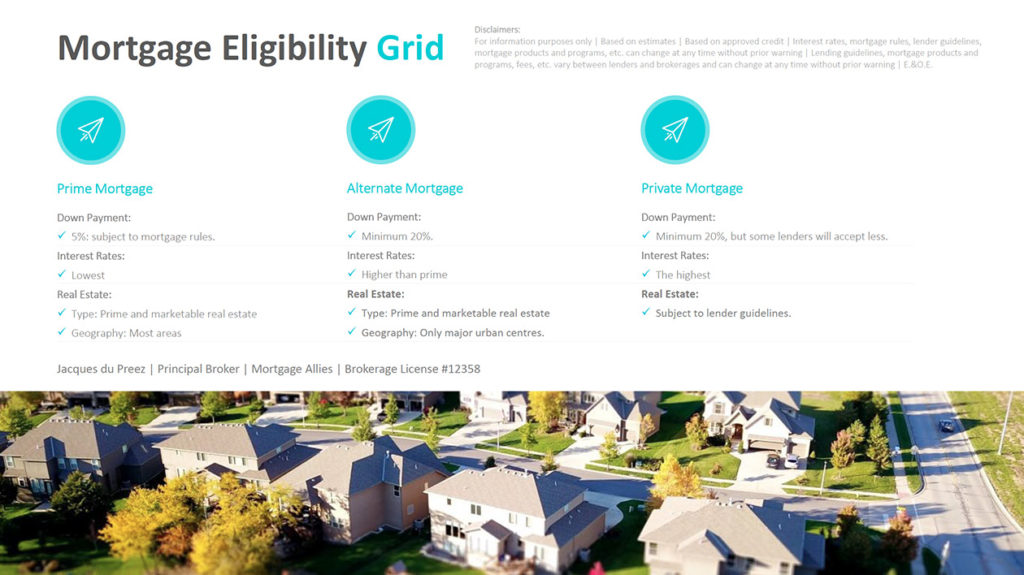

In some ways your credit is more important than your income, because you can still get a prime mortgage if you have great credit, but you lack in income. However, if your credit is damaged, even if you have great income, you will most likely not be able to qualify for a prime mortgage.

- The higher your credit score, the better. While some lending programs may accept a lower credit score, try to keep your credit score above 720.

- Keep at least two active credit facilities and let them each be at least two years old. The older your credit facilities are, the better.

- Pay your debts on time, every time, and do not miss payments.

- Maintain a credit mix. E.g. A credit card and a line of credit instead of two credit cards.

- Keep your balances less than 35% of your credit limits.

- Limit the amount of times per year you allow your credit report to be accessed.

- If you miss payments, contact the lender quickly and explain your situation.

- Don’t depend entirely on installment loans (for example a car loans etc.) to build your credit long-term, because your credit will diminish or collapse once you have paid off the loan.

- Free credit reports and/or credit scores obtained by yourself, may be somewhat helpful to you, but considered these for information purposes only. Lenders will only accept credit reports checked by themselves or by an authorized third party such as a mortgage broker for mortgage application purposes. You should not depend on loan decisions, interest rate offers, etc. from lenders or brokers before your credit is checked and your loan is approved by the lender.

- Your Social Insurance Number (SIN) is not required to check your credit, but the vast majority of lenders will not grant you a loan without your SIN. Be very careful who you give your SIN to, however providing your SIN to a trusted mortgage broker upfront can go a long way to ensure your credit report is accurate.

If you do decide to close a credit facility, make sure that you do the following:

- Pay all interest that may be due from a paid-off balance before you close and forget about the facility. Not doing this may put you in arrears and damage your credit.

- Insist that the lender provides you confirmation, in writing, that it has closed your account and it has stopped reporting to the credit reporting agencies.

Creating a budget is very important when it comes to managing your credit. download our free budgeting tool below.

Complete the form below to download the FREE Budget like a Boss TOOL

Complete the form below to download the FREE Budget like a Boss TOOL

Thank you to everyone who joined our webinar for the live session. As always, we love the opportunity to connect with you, to share our knowledge, and to hear and answer your questions. We’re looking forward to the next webinar already!