Some Rules for Foreign Purchasers in Canada

Now that we’ve covered the content for those who are new-to-Canada, we’re going to talk through foreign purchasers.

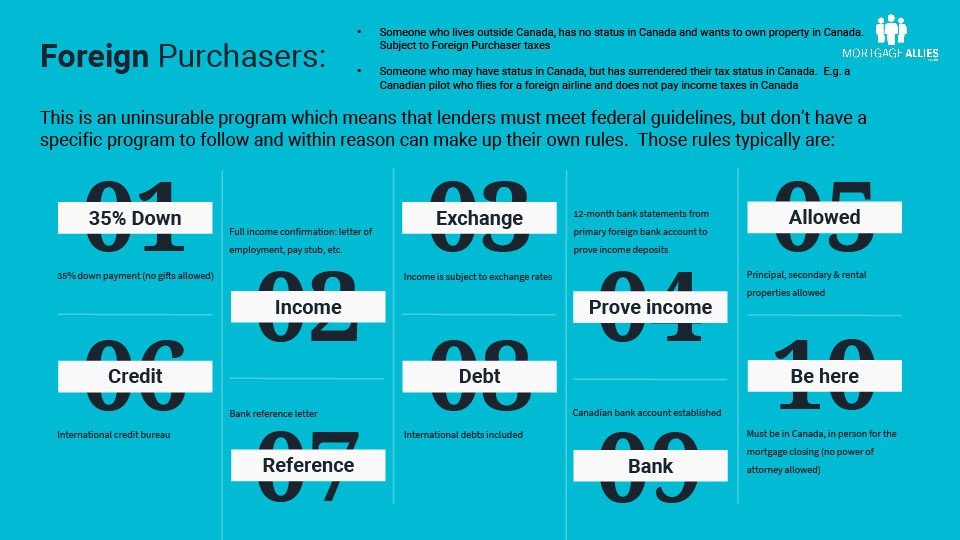

A foreign purchaser who lives outside Canada, has no status in Canada and wants to own property in Canada. He or she will be subject to Foreign Purchaser taxes. A foreign purchaser can also be someone who may have status in Canada but has surrendered their tax status in Canada. For example, a Canadian pilot who flies for a foreign airline and does not pay income taxes in Canada.

This candidate falls into an uninsurable mortgage program, which means that lenders must meet federal guidelines, but don’t have a specific program to follow.

The rules for a foreign purchaser typically are that he or she must be able to put down 35% of the purchase price. Unfortunately, no “gifts” are allowed in this category. The purchaser will need to show full income confirmation in the form of a letter of employment or a pay stub, for example.

Income for this candidate is subject to change concerning interest rates, and this needs to be noted. The borrower will need to present 12-month bank statements from his or her primary foreign bank account to prove income deposits. For the individual operating in this category, principal, secondary and rental properties are allowed.

The other items needed are a statement from the international credit bureau, a bank reference letter, the inclusion of all foreign debts, an established Canadian bank account, and lastly there is no power of attorney allowed, so the purchaser must be in Canada for the closing of the mortgage.